Everyone's talking about agentic commerce. Nobody agrees on what it means.

Updated on

If you’ve followed retail and AI over the past year, you’ve heard the phrase agentic commerce roughly a thousand times. What you may not have noticed is that the people using it aren’t describing the same thing. A payments executive from Stripe, a luxury brand’s digital director, and an OpenAI product manager will each give you a confident definition, and those definitions barely overlap.

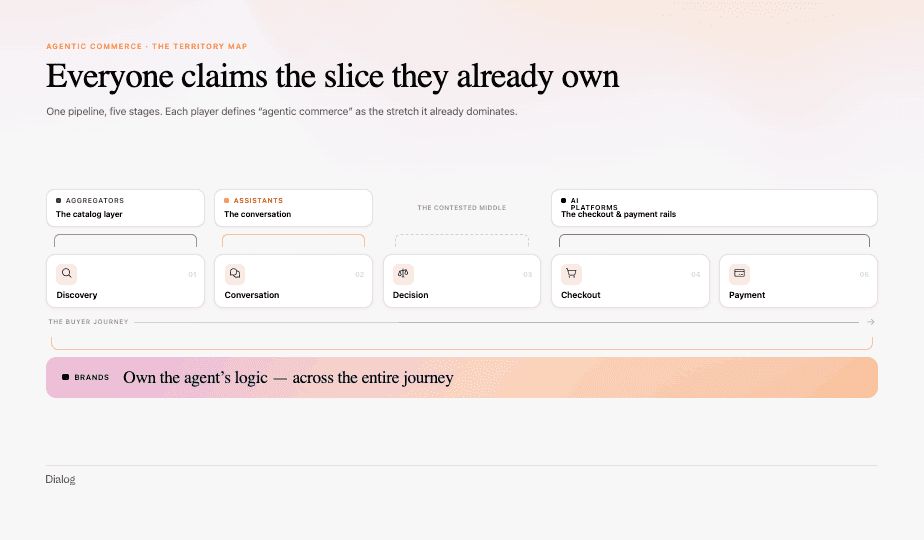

That’s not a sign the term is empty. It’s a sign that “agentic commerce” is being defined, in real time, by whoever stands to win from their particular version of it. Each player draws the boundary around the part of the value chain they already control, or wish to control. We spend our days inside that chain, so here’s an honest map of the definitions competing for the word, and the question they’re all quietly circling: who ends up owning the customer.

1. The checkout definition

The loudest definition was coined first by the major AI platforms. For them, agentic commerce is essentially the moment an AI agent completes a purchase on your behalf. Discovery and conversation are table stakes; the new thing is the transaction.

OpenAI made this concrete in September 2025 with Instant Checkout in ChatGPT, which lets people buy directly inside the chat, starting with Etsy sellers and expanding to Shopify merchants. It runs on the Agentic Commerce Protocol, an open standard co-developed with Stripe. Google answered with its Agent Payments Protocol, then the broader Universal Commerce Protocol in January 2026, and at Google I/O in May 2026 it tied the pieces together with Universal Cart: a single cart spanning Search, Gemini, YouTube and Gmail that brings native checkout across Google’s AI surfaces. In both cases, the idea is to define a common way for agents and payment providers to interact. But for a protocol to truly take off, it must become a widely adopted standard, implemented by every new AI agent and payment provider. Google and OpenAI each pushing their own version has slowed broader adoption, even if the lines are already blurring, with Stripe, for instance, sitting in both camps. [1] [3] [4]

It’s worth noticing that Google’s vision of agentic payments is embedded in a more ambitious one: the Universal Commerce Protocol, which tries to define a standard for the entire buyer journey.

On the payment-provider side, especially among participants in the protocols above, agentic commerce is sometimes reduced to a single step: authorizing an AI agent to validate a payment. Stripe’s Shared Payment Token, introduced for ACP, lets ChatGPT act as an intermediary by passing the merchant a one-time token scoped to that merchant, amount, and time window. The agent can then complete the purchase without either side ever handling the buyer’s raw payment credentials, which remain vaulted with Stripe. For payment providers, this is what agentic commerce is about: securing payments in an internet ruled by agents. [2]

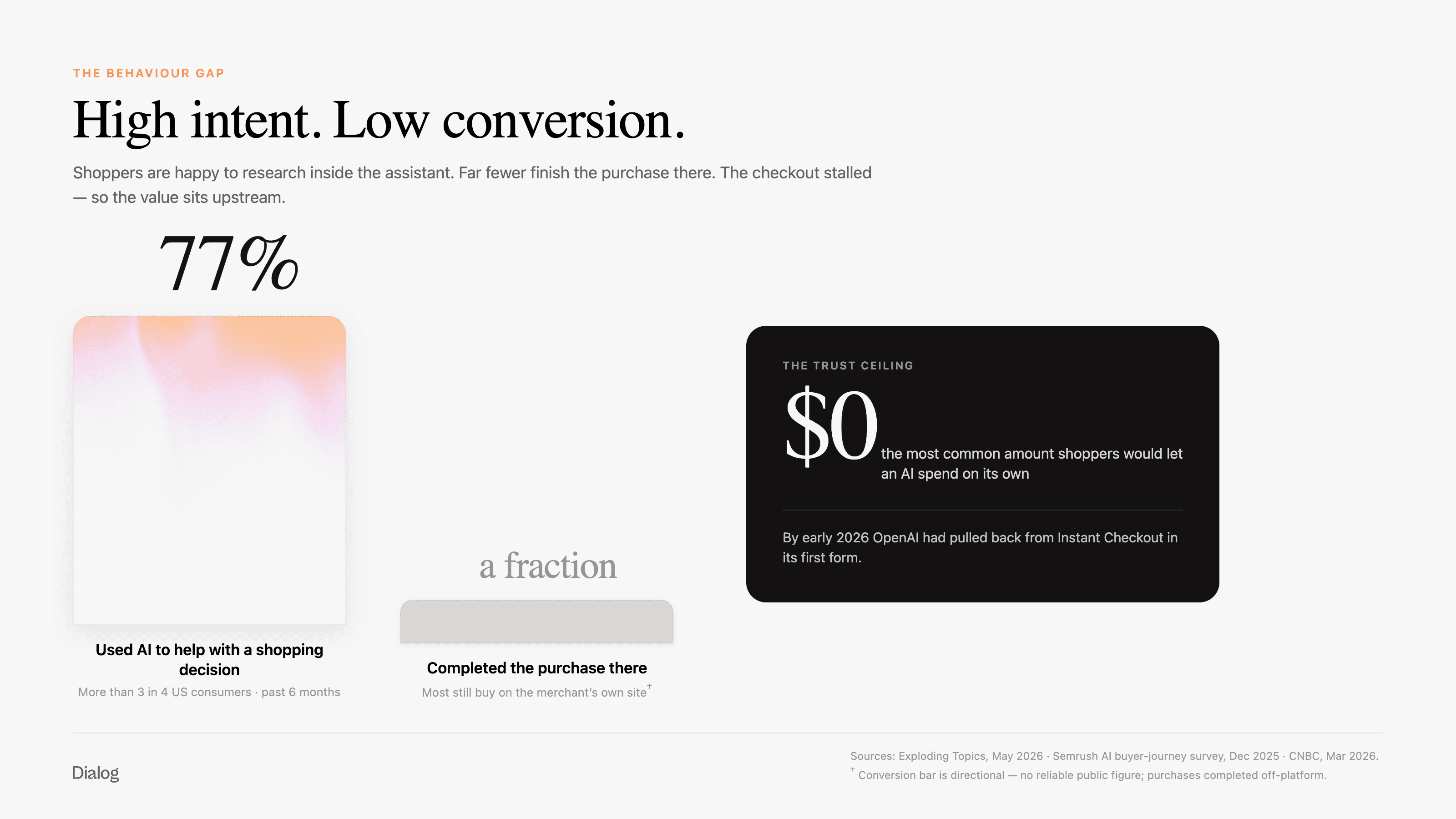

In practice, the results aren’t here yet. By early 2026, OpenAI had pulled back from Instant Checkout in its first form. Reporting from CNBC described a company that had struggled to onboard merchants (only a few dozen of Shopify’s millions ever went live, and as of February 2026 OpenAI still hadn’t built a system to collect and remit US sales taxes), to surface accurate product data, and to ship basics like multi-item carts and loyalty. Shoppers were happy to research products inside ChatGPT but completed the actual purchase elsewhere: high intent, low conversion, as one post-mortem put it. OpenAI’s response was telling: let merchants use their own checkout, and refocus its own effort on product discovery, describing what you want, uploading an image, setting a budget. A quiet admission of where the value could really sit for brand and end user. [5]

2. The assistant definition

Which is why the platforms don’t stop at the pipe. When introducing UCP, even while focusing on checkout and payments, Google still framed discovery as central to where this is heading. On OpenAI’s side, the focus on discovery has been there from the beginning, via raw product data, and now enriched through ChatGPT Apps, which let a business deliver a more branded experience directly inside the assistant.

The behavioral shift is real and measurable. More than three in four US consumers say they’ve used AI to help with a shopping decision in the past six months (Exploding Topics, May 2026). In a December 2025 Semrush survey of US shoppers, 38% said they use AI tools specifically for product research and 30% to compare options side by side, with ChatGPT the most-used tool at 64% monthly reach. Pew data, meanwhile, puts shopping at only about 2% of all ChatGPT prompts, but at ChatGPT’s scale that’s still on the order of 50 million shopping-related queries a day. Being able to ask a question directly and get a recommendation that feels personalized is, evidently, compelling. [6] [7]

For brands, the picture is more open-ended than settled. It’s still genuinely hard to see how a general-purpose assistant explores a category and decides which products to surface. And the playbook for showing up, what some now call GEO (generative engine optimization), is young and can shift with any model release. Google, OpenAI and Anthropic each address part of this through ChatGPT Apps and MCP, which let a brand expose some of its own logic to the agent rather than be paraphrased by a generic one.

None of this makes the assistant a dead end; it’s a genuine acquisition channel. But it isn’t replacing the brand’s own site either. Discovery increasingly starts in the assistant while conversion still tends to land on the merchant’s surface, and consumers are explicit about the limit: in that same research, the most common amount they’d let an AI spend autonomously was $0. The type of purchase matters too: utilitarian, low-stakes buys lend themselves to the assistant, while considered, technical or pleasure-driven purchases are far likelier to continue through a brand’s own channels. Just as strong brands survived Amazon and Google Shopping didn’t kill e-commerce, the best brands will find their place here without handing their data to AI labs.

3. The brand-owned definition

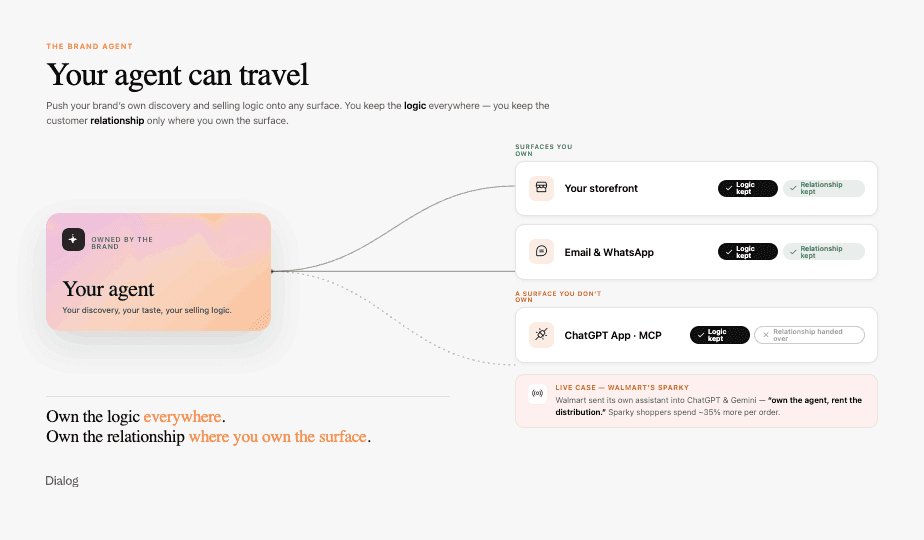

Then there’s a camp that rejects the premise of the first two: the agent shouldn’t be someone else’s. Its definition has less to do with where the agent runs than with who owns it. What matters is that the brand owns the agent’s logic: how it discovers products, the tone it speaks in, how it sells, and, wherever possible, the customer relationship that logic creates.

The purest expression of that is the brand’s own storefront, where you own both outright. And “intelligent storefront” itself splits into two very different things worth separating.

The first is the conversational layer: a brand-specific agent embedded in the site that answers questions, recommends products, and guides you toward a decision; an in-store associate you can talk to. This is where we work, at Dialog: agents trained on a brand’s own data, placed across the homepage, product pages, and search, instead of a chatbot bolted into the corner.

The second is the experience layer, or generative UI: the interface itself reconfigures around intent. Rather than a chat window sitting on top of fixed pages, the page is the response. Brunello Cucinelli’s Callimacus platform, built with its in-house venture Solomei AI, is the showcase: a “pageless,” intent-led site where a multi-agent system reads what you’re after and assembles the layout in real time. The part most coverage skips: building both well at once is genuinely hard, and the brands that fuse them will have something neither the platforms nor the aggregators can easily copy. [8] [9]

But the storefront is only the home base. The same brand-owned logic can travel. Push it into channels the brand already owns (email, WhatsApp, messaging) and you keep both the logic and the relationship, just on a different surface. Push it onto surfaces you don’t own (a ChatGPT App, an agent reached over MCP) and the brand can still show up as itself, with its own discovery and selling logic, rather than as a paraphrase inside a generic assistant. Walmart is the clearest live example: when OpenAI’s Instant Checkout stalled, it refused to sit in ChatGPT as a product feed and instead made its own assistant, Sparky (launched June 2025), travel into ChatGPT and Gemini, a posture observers summed up as “own the agent, rent the distribution” (Sparky shoppers reportedly spend about 35% more per order than non-users). The trade is still real: on a surface you don’t own you keep the logic but usually hand over the relationship, even if Walmart’s scale let it hold onto more than most. The rule of thumb is simple: own the logic everywhere; own the relationship wherever you own the surface. [10] [11]

Either way, this definition is almost the inverse of the platform one. The platforms want the agent to meet you in ChatGPT and route a transaction back to the merchant. This camp wants the agent to be the brand (its discovery, its taste, its judgment) so the brand is never reduced to a line item in someone else’s feed. For premium especially, where the experience is the product, that distinction is existential.

4. The aggregator definition

Finally, the catalog layer. Here, agentic commerce is a universal product index that sits above all merchants: the new front door to shopping. An aggregator can be any company that already has access to a large number of e-commerce catalogs, such as a large marketplace (Amazon), an e-commerce engine (Shopify with all the catalog they own), or a consumer-facing app (for instance, Joko in France).

The hard part of shopping was never paying; that problem was solved years ago. The hard part is the twenty open tabs, the compromises, the “good enough” that closes the browser. That’s where the friction lives, and it’s where nobody was building. The demand, in other words, sits above where the rails were being built. The bet here is that an agent is only as good as the data it can reach, and without a clean, queryable, cross-merchant catalog, every shopping agent is stuck crawling fragile websites or living inside a single retailer’s walled garden. The durable play is to become that layer: unified inventory, real-time availability, pricing across merchants, all in one place.

Joko, a French startup building a personal shopper for end users, is a clear instance of this evolution. Starting from cashback and price tracking, it is now building exactly that kind of unified catalog, and its founder reads OpenAI’s retreat from checkout as confirmation that the real frontier was always one step earlier, at discovery. [12]

He’s right about the frontier, which is exactly why this camp is worth watching. Amazon’s trajectory shows how powerful, and how contested, the layer is: its Rufus assistant, folded into “Alexa for Shopping” in May 2026, now includes a “Buy for Me” capability that completes purchases on sites Amazon doesn’t even own, a move that has already drawn pushback from retailers who never agreed to be bought from on their customers’ behalf. Whoever controls discovery is positioned to control everything downstream of it. [13]

But notice what “discovery-led” means here. The aggregator’s answer to finding being the hard part is to become the place where finding happens, one trusted front door across every merchant. Discovery does run on trust and real personalization; the question is whose brand earns that trust. In this model it’s the aggregator’s, and each merchant slides back into being catalog data underneath it. The platforms reduce the brand to a line item at checkout; the aggregator can do the same thing one step earlier, at discovery.

We believe this Amazon-led version is here to stay: the natural evolution of the Amazon Marketplace into the agentic era.

Why the definitions don’t line up

Put these side by side and a pattern appears. Each player defines agentic commerce as the slice of the journey they already dominate:

AI platforms → the checkout moment, and the payment rails beneath it

Assistant makers → the conversation

Brands → owning the agent’s logic and the customer relationship

Aggregators → the discovery and catalog layer

None of them is wrong. They’re describing different stretches of the same emerging pipeline, and quietly arguing about who gets to own the customer relationship at the end of it. That’s the real fight hiding inside the vocabulary.

For now, the useful move isn’t to pick the “correct” definition. It’s to acknowledge that agentic commerce is a very large territory, claimed by very different actors who each cast themselves as the leader of their own slice of a broader whole, and then to ask the question all of them are circling: when an agent does the shopping, whose agent is it?

On our side, we believe brands must own their agent, and there’s much more to say about the “brand agent.” But that deserves its own piece. That’s the next one.

Sources

[2] Stripe, “Instant Checkout, ACP and Shared Payment Token”

[4] The Next Web, “Universal Cart and AP2 at Google I/O 2026”

[5] CNBC, “OpenAI agentic shopping, Etsy, Shopify, Walmart and Amazon”

[8] makemepulse, “Brunello Cucinelli AI shopping experience”

[9] TheIndustry.fashion, “Brunello Cucinelli launches AI-enabled e-commerce platform”

[11] Digital Commerce 360, “Walmart Sparky agent AI sales and supply chain”

[13] Retail Dive, “Amazon Alexa for Shopping and Buy for Me”

FAQ

Why does everyone define agentic commerce differently?

Each player defines agentic commerce around the part of the value chain they already control. A payments company like Stripe frames it around checkout infrastructure. A platform like OpenAI or Google frames it around the assistant layer. A brand frames it around owning the customer relationship. The definitions aren't wrong, they're self-interested, and none of them fully agree.

Who owns the customer relationship in agentic commerce?

That's the open question behind every definition of agentic commerce: when an AI agent does the shopping, whose agent is it, the platform's, the payment provider's, or the brand's? Whoever's agent it is ends up owning the customer relationship, which is why brands are increasingly building and controlling their own AI shopping agent rather than depending on a third-party assistant.

What is agentic commerce?

Agentic commerce describes AI agents making or assisting purchase decisions on a shopper's behalf. The term has no single agreed definition: payment providers frame it as one-click checkout, AI platforms frame it as a shopping assistant inside a chat interface, brands frame it as their own AI selling on their own site, and marketplaces frame it as an aggregator that transacts across many brands at once.